Structural Trends in Gold Supply

One area receiving increased attention is the pace of new gold discoveries.

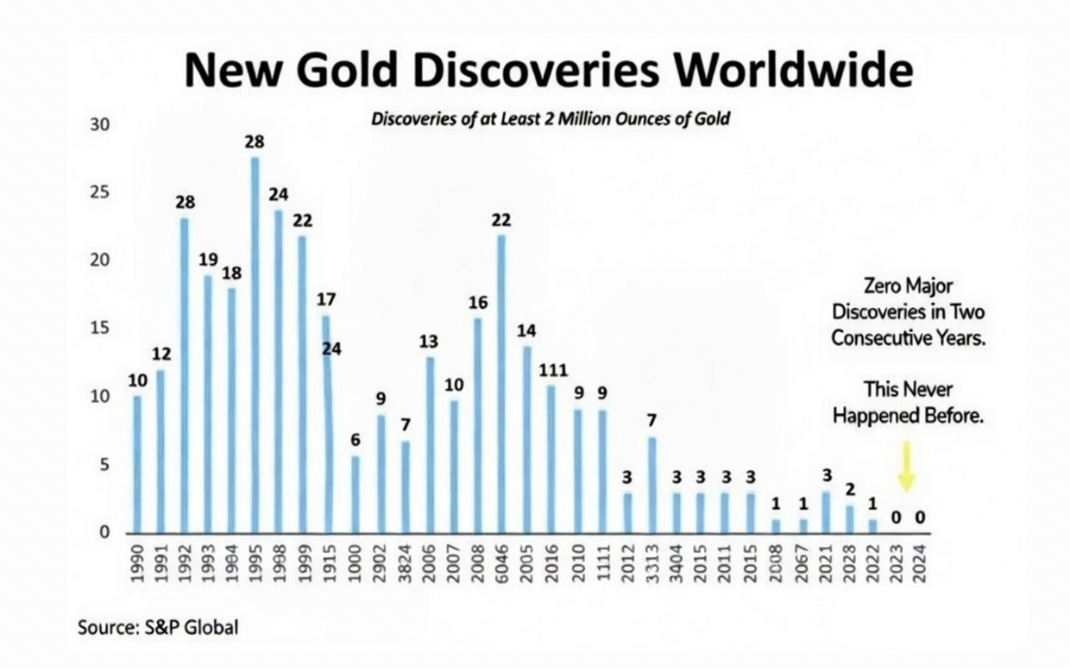

Industry data shows that large-scale gold discoveries (often defined as deposits exceeding two million ounces) have declined compared with levels seen in the 1990s and early 2000s. In recent years, the number of significant discoveries has fallen to low single digits, with some years reporting none of that scale.

While exploration continues globally, the trend suggests that bringing new large deposits into production has become more complex, capital-intensive and time-consuming.

At present, global mine production is approximately 3,000 tonnes per year. Annual output fluctuates depending on mining investment, energy costs, regulatory frameworks and ore grades. Although supply is finite, production can still respond over time to sustained price incentives.

Scarcity is one factor influencing the gold market but it operates alongside demand conditions, monetary policy and investor behaviour.

Demand Considerations

On the demand side, central banks have increased gold purchases in recent years relative to longer-term historical averages. Reserve management strategies differ by country and can evolve depending on currency exposure, trade balances and geopolitical considerations.

Private investors have also shown varying levels of interest in gold, particularly during periods of inflation uncertainty or financial market volatility. However, investor demand can be cyclical and is sensitive to real interest rates, currency strength and broader risk appetite.

Gold has experienced both extended periods of appreciation and periods of consolidation or decline over the past several decades. Past performance is not a reliable indicator of future results.

Market Context and Risks

While constrained discoveries may influence long-term supply dynamics, gold prices are also affected by:

For example, sustained higher real yields can reduce the relative attractiveness of non-income-producing assets. A stronger dollar can also influence global demand patterns. Likewise, shifts in central bank buying trends could alter market momentum.

Gold does not produce income and can experience price volatility. As with all assets, returns are not guaranteed and market conditions can change.

Portfolio Considerations

Gold has historically been used by some investors as part of a diversified portfolio, particularly during periods of monetary expansion or elevated inflation. Others hold it as a long-term store of value alongside other asset classes.

Certain UK legal tender coins are currently exempt from Capital Gains Tax for UK residents. Tax treatment depends on individual circumstances and may change.

Investors may wish to consider how physical gold aligns with their broader financial objectives, time horizon and risk tolerance.

If you would like to discuss whether physical gold forms part of a balanced long-term approach, you are welcome to contact Roman Brothers on 0208 080 2848 for further information.

The value of gold can rise as well as fall, and investors may receive less than they originally invested. Past performance is not a reliable indicator of future results. This communication is for information purposes only and does not constitute personal investment advice. Tax treatment depends on individual circumstances and may change.